CHANGED BACKDROP

The lending environment has changed dramatically over the last twelve months. However, with financial markets stabilising after a period of volatility, enquiries for big ticket lending deals are now coming back. The industrial & logistics sector is still regarded favourably by lenders, but borrowers need to consider a range of new risks and opportunities in the current market.

Download our Industrial & Logistics Market 2023 report →

HIGHER RATES

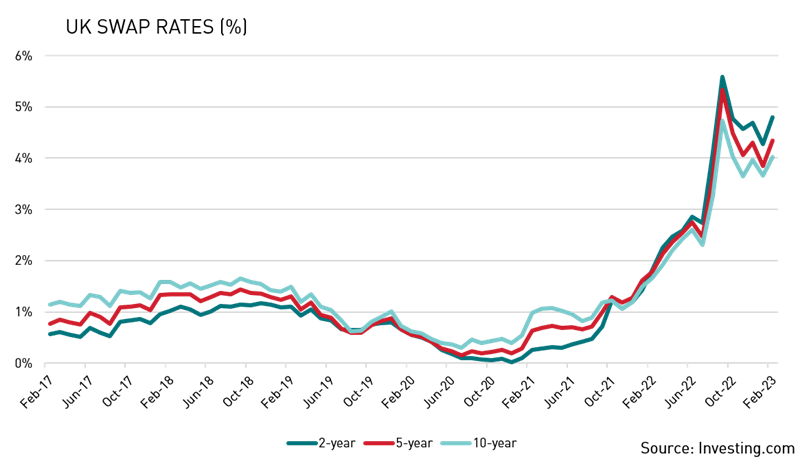

Hikes to the Bank of England base rate and wider financial market volatility have driven huge increases in the cost of 2, 5 and 10-year swaps over the last 12 months. A 5-year swap was priced at c. 4.34% at the end of February 2023, compared with c. 1.79% a year earlier. While this is lower than the peak of c. 5.50% reached in the aftermath of last September’s mini budget, it still represents a dramatic shift in pricing.

Rising rates have had a direct impact on the ability of borrowers to service loan repayments, as they have led to significant increases in the overall cost of funds. The total interest rate on a 5-year lending product for a prime industrial asset has risen from a low of c. 2.29% in January 2021 (5-year swap at 0.29% + 2.00% margin) to c. 6.34% in February 2023 (5-year swap at 4.34% + 2.00% margin). This has restricted affordability and forced lenders to exercise greater caution when analysing requests for finance.

SHIFTING TERMS

With longer-term swap rates now lower than short-term rates, there is an argument for sourcing finance options that allow borrowers to fix rates for 10 years. This comes with its own challenges, as lenders need to be comfortable with tenancy risks, lease lengths and expectations for property values at the end of the 10-year period. However, with margins remaining relatively consistent, there could be a cost advantage in acquiring 10-year finance and then holding through the more uncertain market conditions.

For borrowers seeking longer-term finance, lease-concurrent lending may be available, with finance options of 10+ years achievable. The existence of this type of deal is not widely known, but lenders are increasingly prepared to offer this for the right assets with the right tenants.

RETURNS ERODED

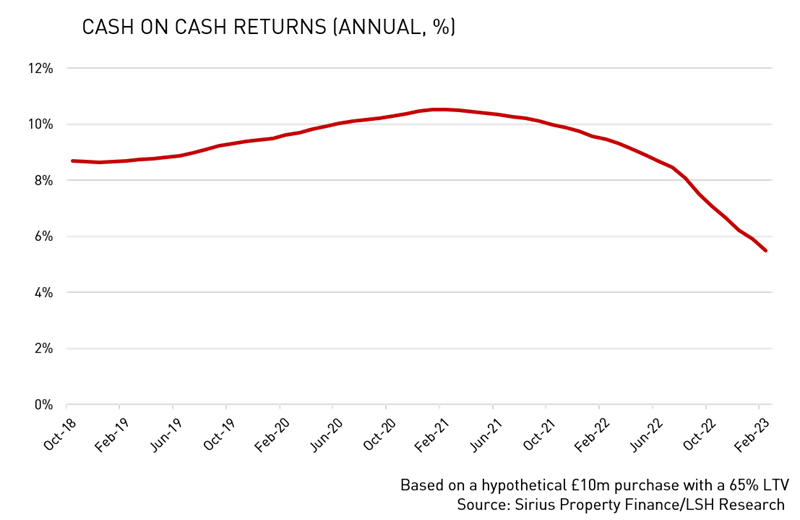

The increase in the overall cost of finance has had a direct impact on cash-on-cash returns, particularly for low yielding assets. When all-in finance costs were c. 2.50-3.00%, there was a clear advantage in incorporating finance into an investment purchase. Those who were able to fix for 5-10 years when rates were low are in an advantageous position now.

However, with the total cost of industrial finance reaching c. 5.00-6.50%, investors borrowing at these rates will see cash-on-cash returns dramatically eroded by increased interest costs. As reduced leverage is available, purchasers will also need to increase the level of equity invested in deals, further dampening cash-on-cash returns.

We estimate that annualised cash-on-cash returns have close to halved since two years ago. Overseas purchasers with cash-on-cash return targets of c. 8% will no longer be able to source appropriate finance to achieve their aims unless asset prices decrease.

LTVS DOWN

In addition to higher interest rates, lending terms have also been affected by a lowering of LTVs, stemming from lenders’ increased perceptions of risk. The easiest way for lenders to accommodate higher risk is to reduce LTV levels across all asset classes, thus limiting their exposure to potential falls in property values and market fluctuations. As a result, we have typically seen LTVs decrease from 70% to 65% in the investment space; and from 80% to 70% in the development finance sector.

Lower LTVs and higher interest rates will be of particular concern to investors that have opted for variable rate finance, shorter fixed terms, or with finance soon to reach expiry/renewal, as they will not be able to refinance on like-for-like terms.

OPPORTUNITIES FROM DISTRESS

Lower LTVs create specific risks for borrowers needing to refinance. If, for example, a borrower has a loan maturing at 70% leverage, and they can only secure 60% leverage in the current market, there is 10% equity gap that needs to be filled. Given the uncertain market conditions, we have seen lenders become increasingly inflexible and put growing pressure on borrowers to fill the gap.

In these circumstances, borrowers will need to either inject additional equity into the refinancing, or to seek alternative options with another lender. If they are unable to do this, there is a risk that loans will be defaulted.

Borrowers may opt to sell assets quickly at a slight discount to alleviate the pressure placed on them by lenders. As a result, opportunities for distressed asset purchases may be created in the industrial investment market, particularly for secondary and tertiary assets. With higher interest rates more generally putting downward pressure on values, there may be a relatively short window of time during which opportunistic and equity-rich investors are able to take advantage of price reductions and more limited competition for assets.

MARGINS STEADY

While the total cost of funds has greatly increased, lenders’ margins have stayed relatively consistent, and industrial investments have continued to attract the most favourable rates from high street banks, challenger banks and institutional lenders. For prime industrial assets, lenders’ margins are currently in the 1.75-2.50% range, which compares with 2.25-3.50% for prime offices and 4.00%+ for retail.

This reflects lenders’ continued belief that industrial is the most robust commercial property sector, due to strong fundamentals such as tight supply and ongoing rental growth prospects. Other asset types, such as secondary offices and retail are seen as carrying much higher risks for lenders.

Across all sectors, there is a clear movement away from secondary assets, and increased scrutiny is being placed on the liquidity of borrowers, covenant strength, the location and quality of assets and vacancy risks. Lenders are taking a risk-averse approach and considering worst-case scenarios in which they may need to recover loans.

DEVELOPMENT FINANCE RISKS

The rapid growth of industrial development and investment resulted in the asset class being seen as ‘bulletproof’ by lenders in recent years, particularly in prime locations. Lenders were prepared to offer development finance before tenants were secured, recognising that it could be uneconomical to arrange pre-lets prior to construction when rents were rapidly rising and occupiers were readily available.

However, lenders’ attitudes to development finance have now hardened. With take-up slowing, speculative development is seen as carrying higher inherent letting risks and lenders are placing a huge importance on pre-lets and the covenant strength of occupiers entering into pre-let contracts. We are seeing lenders refuse to look at industrial development schemes without a pre-let in place; and the liquidity and experience of borrowers is also playing a key part in lenders’ decisions.

A BETTER OUTLOOK

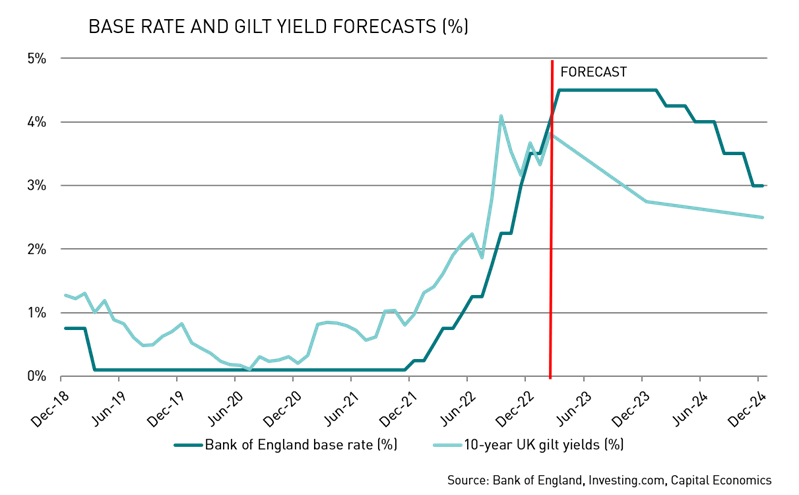

Movements in the Bank of England base rate will play a key role in shaping financial market sentiment over the next 12 months. The market consensus is that the base rate will peak at no higher than 4.50% in H1 2023, and that the Bank will move to cut rates in early 2024.

However, with the outlook for inflation and the wider economy improving, I expect the base rate to come down sooner and faster than the consensus. I believe there is a strong possibility that the base rate will start to move lower in Q4 this year and eventually settle in the 3.00-3.50% range.

A more stable financial backdrop will bring greater certainty to purchasers and developers, and help lenders’ perceptions of risk to become more relaxed. Over the coming months, lenders will once again start to consider secondary assets, and take a more pragmatic approach to weaker covenant strengths and less experienced borrowers. Lenders will also become more open to speculative projects, particularly in key logistics locations, and this should kick-start more development activity.

While the lending market has shifted dramatically over the last 12 months, it is now stabilising and we are already beginning to see an increased volume of enquiries coming through from borrowers. It remains a challenging market, particularly for those needing to refinance, but greater certainty and more favourable lending conditions should emerge as the year progresses.

Download our Industrial & Logistics Market 2023 report →

Ashley Elkin is Senior Associate at Sirius Property Finance. Contact Ashley on ashley.elkin@siriusfinance.co.uk.

Related Content

Get in touch

Email me direct

To:

REGISTER FOR UPDATES

Get the latest insight, event invites and commercial properties by email