What is tocs?

The Total Office Cost Survey (TOCS) is the most definitive independent survey of its type, providing detailed information on office costs for over 50 UK locations.

TOCS leaves no stone unturned, providing figures on a per sq ft and per employee basis across 22 separate cost metrics, ranging from business rates to landscaping to waste management, across both new and 20-year-old office buildings.

This allows office occupiers to:

- Easily view and compare costs between locations

- Check office costs are in line with market rates

- Benchmark their own costs in specific UK locations

- Inform location strategies

TOCS Contributors

-

Accelerator - technology

-

Churchill Group - facilities management

-

GUK - security

-

Kinnarps - office furniture

-

Limpio Office Solutions

-

Oktra - office design & build

-

Sommers Waste Solutions

-

Tricon Foodservice Consultants

-

Urban Planters - office plants

Offering a complete horticultural solution to all things green and plant-related.

Find out more

Viewpoint: Growing Healthy Workplaces, Jane Leese from Urban Planters

-

ZTP - energy management and software

TOCS 2025

Explore costs in your area

View full office occupancy costs across the UK and assess how these differ by location and sector across new and 20-year-old buildings on a per sq ft and employee basis.

Explore costs

MARKET Insight

Industrial and Logistics Market

Explore industrial market take-up, availability, rents, prime land values and key deals across the UK.

Launch app

Methodology

- Components

-

To identify costing, we have analysed all relevant annual and one off capital costs for the occupation of office space. This analysis has taken into account expenditure items contained within the IPD Total Occupancy Cost Code.

Actium Consult, the previous owner of TOCS, helped IPD to define this cost code, which is now established as an industry benchmark. These costs include net effective rents, rates, annualised costs such as maintenance, security and cleaning and relevant business support costs such as reception, telephones, catering and printing and reprographics. - Net effective rent

-

Calculating the net effective rent from the headline rent is a necessary step in calculating the total cost of occupation in different locations around the UK.

For the purpose of this survey, the level of headline (or lease) rent of a hypothetical 50,000 sq ft NIA office building in a prime office location let to a single occupier was determined. It was assumed that this property, excluding car parking, would let within a reasonable time, approximately six months, and on a 10-year FRI lease with a review after five years.

The typical rent free period for each of the 54 centres covered was also taken into account.

Net effective rent is calculated using the current quoted prime rent for a good quality modern office building. The net effective rent reflects any rent free inducement on a straight line basis up to the end of a 10-year lease. The rent free period also includes the traditional three month allowance for fit out. - How is space used?

-

Since the intensity of use in office buildings varies it has become standard practice in the industry when looking at occupancy costs to measure not only price per sq ft but also costs per workstation. For organisations who use a 1:1 ratio for workstations (no desk sharing/hot desking) and staff, this measure also relates to cost per staff member.

Therefore a good best practice benchmark for the total workstation area is 100 sq ft (NIA). This is a reasonable assumption for an occupier moving into and refitting new space, although in practice some occupier sectors use considerably more space and some less.

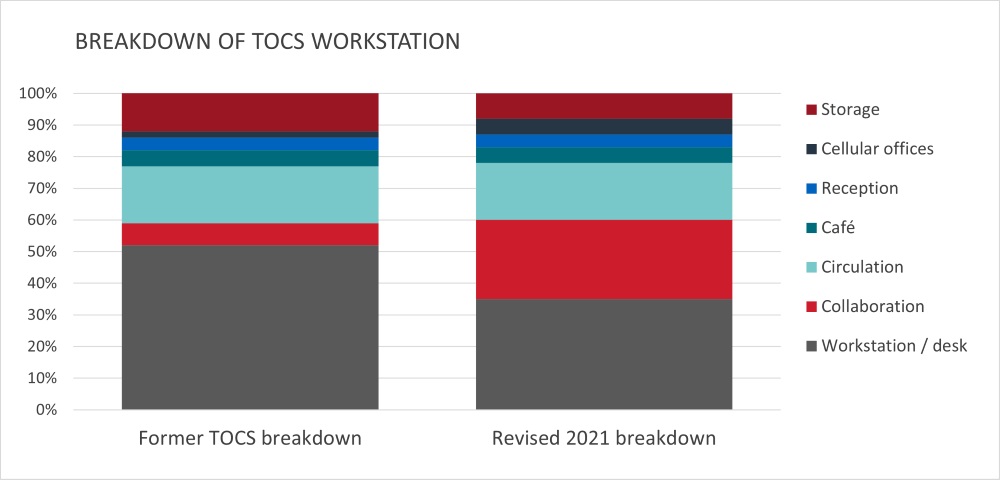

The experience of the pandemic has accelerated shifting trends around office layouts and, in order to reflect this, key changes have been have been put into place relating to the breakdown of the space associated with a typical workstation, as set out below. The net area of a workstation* is the area taken up by a desk and a chair, with changes to the assumptions in the 2021 survey including the scaling down in the number of desk spaces from 500 to 350 in exchange for a greater amount and range of workspaces within the category for collaboration.

Source: LSH RESEARCH

Our space calculation continues to assume approximately 12% cellular space and 88% open plan.

- Definition of cost heads

- Download PDF here

- TOCS methodology and assumptions

-

The cost data has been supplied by Lambert Smith Hampton and a number of leading industry suppliers. The data in this edition represents the position as of June 2025.

To get consistent and comparable costs between locations, the type of building and associated day-to-day services have been specified in detail. For full information on the building's specification, see Definition of Cost Heads below.

Key building parameters:- Provides 50,000 sq ft (NIA), built on four floors in a prime location. The construction includes a steel frame, curtain walling and raised floors.

- There are 500 individually allocated personal workspaces.

- Net effective rents are utilised rather than headline rents as these provide a more accurate reflection of actual costs inclusive of rent free incentives.

- The building is let on a 10-year FRI lease with a rent review after five years.

- The occupancy assessment also assumes good configuration efficiency with primary circulation totalling 20 per cent balance of NIA.

- Ancillary and amenity spaces such as reception, post handling, breakout space, meeting rooms and catering space make up approximately 15 per cent of the total space.

- Procurement

-

We have adopted the hypothetical purchasing power of a medium sized organisation which employs 500 staff, this is considered the minimum size required for procuring the TOCS bundle of services.

The survey has also assumed all expenditure items are procured separately, which in the real world is unlikely.