Forthcoming rises in interest rates will inevitably put further pressure on property pricing. However, property yields are unlikely to move precisely in-step with interest rates, and longer-term structural trends will continue to influence the outlook for the sectors.

Gathering interest

The financial tumult caused by the recent ‘mini-budget’ has put a renewed spotlight on the relationship between interest rates, gilts and commercial property yields.

Rising interest rates were already at the forefront of investors’ thoughts, as a period of historically low rates lasting more than a decade has ended this year, with the Bank of England repeatedly raising the base rate to counter high inflation.

Gilt yields, which are highly correlated with money market rates, have been on an upward path over most of 2022. However, it was not until the middle of the year that property yields appeared to start reacting to changing financial and economic conditions, subsequently softening to varying degrees across the sectors.

Expectations for the near-term path of interest rates have continued to increase, with inflation remaining high and financial markets responding to the mini-budget by selling sterling and UK gilts. Market pricing implies that the Bank of England base rate could reach as high as 6% in 2023. While forward market rates are not always accurate predictors of the future, interest rates appear to be heading towards levels not seen since the early days of the global financial crisis in 2008.

Amid rising interest rates and a weakening economic backdrop, the share prices of listed property companies have already tumbled, with many being down by 30-50% since the start of the year. While transactional pricing has not yet moved by anything like this, some investors are clearly anticipating a significant correction in property values.

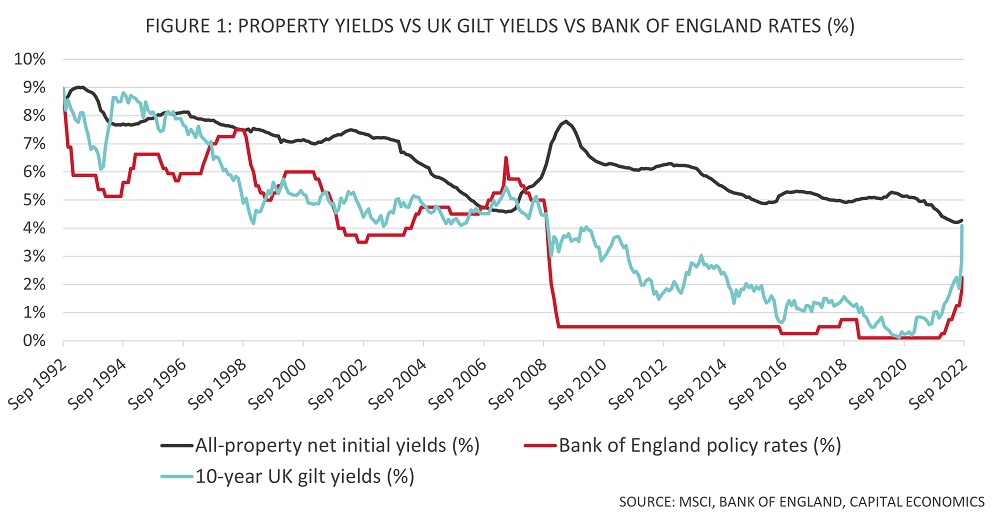

Learning from the past

Conventional wisdom would suggest that rises in interest rates usually lead to upward movements in property yields. This is broadly supported by Figure 1, which plots MSCI’s all-property net initial yield against the Bank of England’s policy rate and 10-year UK gilt yields over the last thirty years. All three have broadly moved in the same direction over the long term, but there have been significant periods when property yields have moved in the opposite direction to interest rates, most notably during the global financial crisis.

Statistically, property yields have a stronger relationship with gilt yields than they do with the Bank of England base rate. Over the last thirty years, the correlation coefficient between the all-property net initial yield and 10-year UK gilts is 0.8 – showing a clearly positive, but by no means perfect correlation, while the correlation with the base rate is 0.6.

The stronger correlation reflects the importance that the gap between gilt and property yields has in investors’ assessments of risk and pricing. In most market conditions, property assets need to provide a margin over theoretically ‘risk-free’ investments such as gilts to justify their additional risk.

The size of the risk premium required by investors has fluctuated greatly over the thirty years shown by Figure 2. In the last decade, the gap between the all-property net initial yield and 10-year gilt yields has largely stayed within the 300-500 bps range. However, these are wide margins by historic standards and have coincided with an unprecedented period of low interest rates and asset yields.

Going further back, when gilt yields were higher, investors have been prepared to accept considerably smaller, or even negative risk premiums. Over a thirty-year period, the average margin between all-property and gilt yields is 236 bps.

Mind the gap

Therefore, there is no simple rule of thumb to say that if gilt yields rise by a certain amount, property yields will also move out by a commensurate figure. A multitude of other factors influence property yields, including market dynamics, tenant covenants, macroeconomic conditions, international capital flows, investors’ asset allocations and longer-term structural trends affecting individual sectors. Strong rental growth prospects, in particular, help to justify lower yields.

The reasons behind movements in interest rates and gilt yields are also important. When central banks raise interest rates to cool economic growth, it is likely that occupier demand for commercial property will be strong and support positive investor sentiment. However, when the root cause of rising rates is supply-side driven inflation, as it is now, this may not be the case.

Sector risks

Long-income annuity-type investments, which can include a multitude of property types, are among those most immediately exposed to the impact of rising interest rates. The record-low yields recently seen for this type of asset have become unsustainable due to rising gilt yields, and some repricing is inevitable for deals to be viable.

With margins to risk-free rates being squeezed to very low levels, yields in the industrial sector are also subject to immediate outward pressure. However, occupier fundamentals remain healthy and long-term structural trends continue to support the growth of the sector. If interest rates were to stabilise in the medium term, allowing pricing to settle, strong investor demand is likely to resume, with positive rental growth prospects allowing buyers to accept relatively modest risk premiums.

Within the office sector, the current pricing pressures are likely to exacerbate the ongoing bifurcation of the market. Prime offices that meet post-COVID occupier demand and ESG requirements will continue to be seen as lower-risk assets. However, increasingly large risk premiums may be required before investors consider buying secondary and tertiary offices that need significant capital expenditure to be brought up to modern standards.

High risk premiums are already priced in across most of the retail sector and, as a result, yields are subject to less immediate pressure. Even if yields do start to soften, the impact on capital values will be smaller than that of similar movements in lower-yielding sectors. The exception to this is the retail warehouse segment, where prime yields have already moved out from the low levels seen earlier in 2022.

Ongoing correction

Property yields will inevitably soften in the coming months, but it would be foolhardy to predict the size and length of the correction given the extremely uncertain and volatile financial backdrop.

History has shown that property pricing is usually slower to react to movements in financial markets than other investment types, as it is a relatively illiquid asset class. There is also evidence to show that property investors will accept reduced risk premiums when gilt yields are higher than they have been in recent years.

A meltdown on the scale seen during 2008/09 seems unlikely, partly because the property sector is considerably less indebted now. However, a long period of cheap finance and low yields is over, and investors will have to adjust to a new paradigm. The quality of underlying assets will be key to preserving value amid changing market conditions.

Related Content

REGISTER FOR UPDATES

Get the latest insight, event invites and commercial properties by email