On 1 April 2023 all commercial properties will be reassessed for business rates based on rental values as at 1 April 2021. At that time the UK was in lockdown with many businesses closed and large parts of the workforce required to work at home. Having to value over two million commercial properties in such circumstances is an unenviable task and could result in considerable scope to challenge the new 2023 rateable values.

Overview

Non-domestic rates, commonly known as business rates, are a tax on the right to use and occupy commercial property and are based upon rental values. Rental values change over time and regular revaluations are undertaken in order to ensure that these changes are reflected in the non-domestic rates occupiers and owners are required to pay. The next revaluation will be the first for six years and will come into effect on 1 April 2023. In England and Wales rateable values from this date will be based upon rental values as at 1 April 2021 and in Scotland 1 April 2022.

The Valuation Office Agency (VOA) in England and Wales and the Assessors’ Office in Scotland are responsible for valuing in the order of 2.4m rateable properties with a combined rateable value of £73.5bn. Current rateable values are based on rental values as at 1 April 2015 and since this date there have been several unprecedented events which have impacted property values including Brexit and the Covid-19 pandemic.

Fluctuating rental values

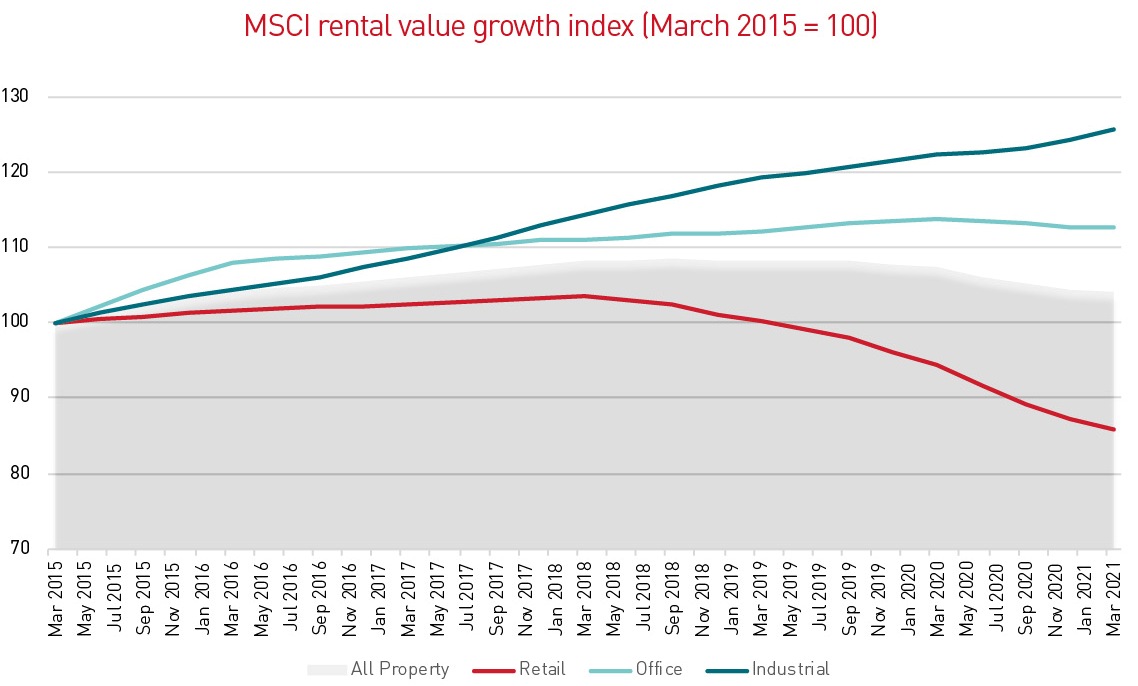

According to MSCI data, on average rental values for all properties increased in the order of 5% between April 2015 and April 2021. As illustrated in the graph on the right hand side, the same data also shows that retail values have fallen over this period by approximately 15%, whilst industrial values have increased in the order of 25%. This should come as no surprise bearing in mind the fall in demand for retail properties both before and during the pandemic, and the corresponding increase in demand for properties in the industrial and logistics sector.

The purpose of any rating revaluation is to rebalance the business rates paid by occupiers and owners of commercial property. If the rateable value of a property increases above the average movement in rental values for all properties across the country as a whole, the rates liability for that property will increase. Conversely, if the rateable value of a property following the revaluation is below the average movement in rental values for all properties, the rates liability for that property will fall. If the results of the forthcoming revaluation follow the MSCI data, any property that experiences an increase in value above 5% will attract a higher liability as a result of the revaluation and anything below that figure will see a reduction in liability.

Profound impact for retail & industrial

This means that across the retail sector as a whole, properties should see a reduction in rates liability in the order of 20%, whereas the industrial sector will experience an increase in the order of 20%. The relative impact of the revaluation between the retail and industrial sectors could therefore be 40%. The MSCI data also suggests the office sector has experienced an average increase in rental value of approximately 12.5% between April 2015 and April 2021. Of the three main property sectors, this level of growth is the closest to the average for all properties and suggests the impact of the revaluation will not be as profound for offices as it is for retail and industrial properties.

Source: MSCI, LSH Research

Although the average movement in rental values across all properties and individual sectors provides an insight into what the overall impact of the rating revaluation might be, the actual level of rental movement for different sectors and locations will vary greatly. For example, Lambert Smith Hampton’s research suggests rental growth for industrial properties in certain parts of London has been in excess of 80% between April 2015 and 2021. If the new 2023 rateable values reflect these levels of rental growth there will be some significant increases in liability for such properties in these locations.

What about other properties?

For those properties that are rarely if ever let in the open market, the VOA values these based on either the cost of constructing a replacement building or the trading performance of the property. Properties that are valued based on construction costs include schools, hospitals, universities and properties occupied by the emergency services. The significant increase in the cost of labour and building materials between 2015 and 2021, suggests that rateable values will increase for properties valued on this approach.

Properties valued on trading performance include hotels, pubs, bingo halls and marinas. As the majority of these properties were unable to trade due to Covid-19 restrictions in place at the 1 April 2021 valuation date, there is an argument to suggest that such properties should attract a nil or nominal rateable value at the forthcoming revaluation. The VOA is highly unlikely to accept such an argument but may, nevertheless, adopt significantly lower values for the leisure and hospitality sectors to reflect the impact of the pandemic.

Challenge of the office sector

The office sector will also present a real challenge for the VOA at the 2023 revaluation. On 1 April 2021, where possible people were required to work at home. Office workers were most likely to be able to follow these restrictions thereby suppressing demand for office accommodation. Furthermore, social distancing guidelines in place at the valuation date meant that even when occupied, offices could only operate at a fraction of full capacity. With this in mind, the rateable values for offices from 1 April 2023 may be lower than the rental indices suggest.

Other factors

The new 2023 rateable values are not the only factor that will affect rates liabilities from next April. Each year the multiplier used to calculate the rates payable for individual properties can be increased by up to the rate of inflation in the preceding September. With inflation predicted to reach in excess of 10% later this year, this could result in a substantial increase in liability even for properties where the rateable value has remained the same or reduced as a result of the revaluation.

Furthermore, at previous revaluations a transitional scheme has been introduced to soften the impact of substantial increases in liability. Such schemes have been self-financing meaning those ratepayers expecting significant falls in liability having to subsidise those who should be experiencing significant increases. If a similar scheme is introduced at the 2023 revaluation, ratepayers in the industrial and logistics sector are likely to be subsidised by those in the retail sector. The full details of any such scheme will not be known until the end of 2022.

Each property is unique

Although rental trends and other factors such as the increase in construction costs can provide an indication of what the impact of the forthcoming revaluation will be for a particular sector and location within the UK, each property is unique. Rental values for a particular building can deviate significantly from the local trend and a low valuation for the 2017 rating revaluation could result in a much higher increase in 2023 than may be expected. Expert rating advice is therefore required to provide a more accurate impact assessment of the 2023 revaluation for individual properties or portfolios.

Related Content

Get in touch

Email me direct

To:

REGISTER FOR UPDATES

Get the latest insight, event invites and commercial properties by email